Macroeconomic and Market Overview

2024 was a year of economic resilience, political turbulence, and strong financial market performance in the United States. Despite persistent fears ranging from recession to revolution, when all was said and done, a balanced portfolio consisting of 60% S&P 500 and 40% Aggregate Bond provided a total return of more than 15%. Again, we are reminded of the importance of maintaining a diversified, long-term investment strategy and the potential pitfalls of market timing based on short-term predictions or political events.

Investors seemed to care most about just three things in 2024: a stronger-than-expected economy, artificial intelligence (AI), and former President Donald Trump’s re-election. Gross Domestic Product (GDP) growth for the year was approximately 2.7%, although as the year went on it accelerated, driven by strong consumer spending, robust job creation, and massive investment in key sectors like technology (AI) and manufacturing. Meanwhile, the labor market remained solid, though there were signs of softening late in the year, as the unemployment rate crossed back above the 4% threshold for the first time since 2021. Inflation continued its downward trajectory, with the Consumer Price Index (CPI) slowing to 2.7% in November, near the lowest level in more than three years. In response, the Federal Reserve (Fed) initiated a new monetary easing cycle in September, announcing its first interest rate cut since the Covid pandemic began. By year-end, the Fed had cut the Federal Funds Rate two more times, to a range of 4.25-4.50%.

The 2024 presidential election was the defining political event of the year. Donald Trump reclaimed the presidency, with – ironically, given headline US economic strength – economic concerns playing a crucial role in the outcome. Regardless, given his longstanding policy of lowering corporate taxes and reducing regulation, his election only further ignited the stock market melt-up that had begun earlier in the year.

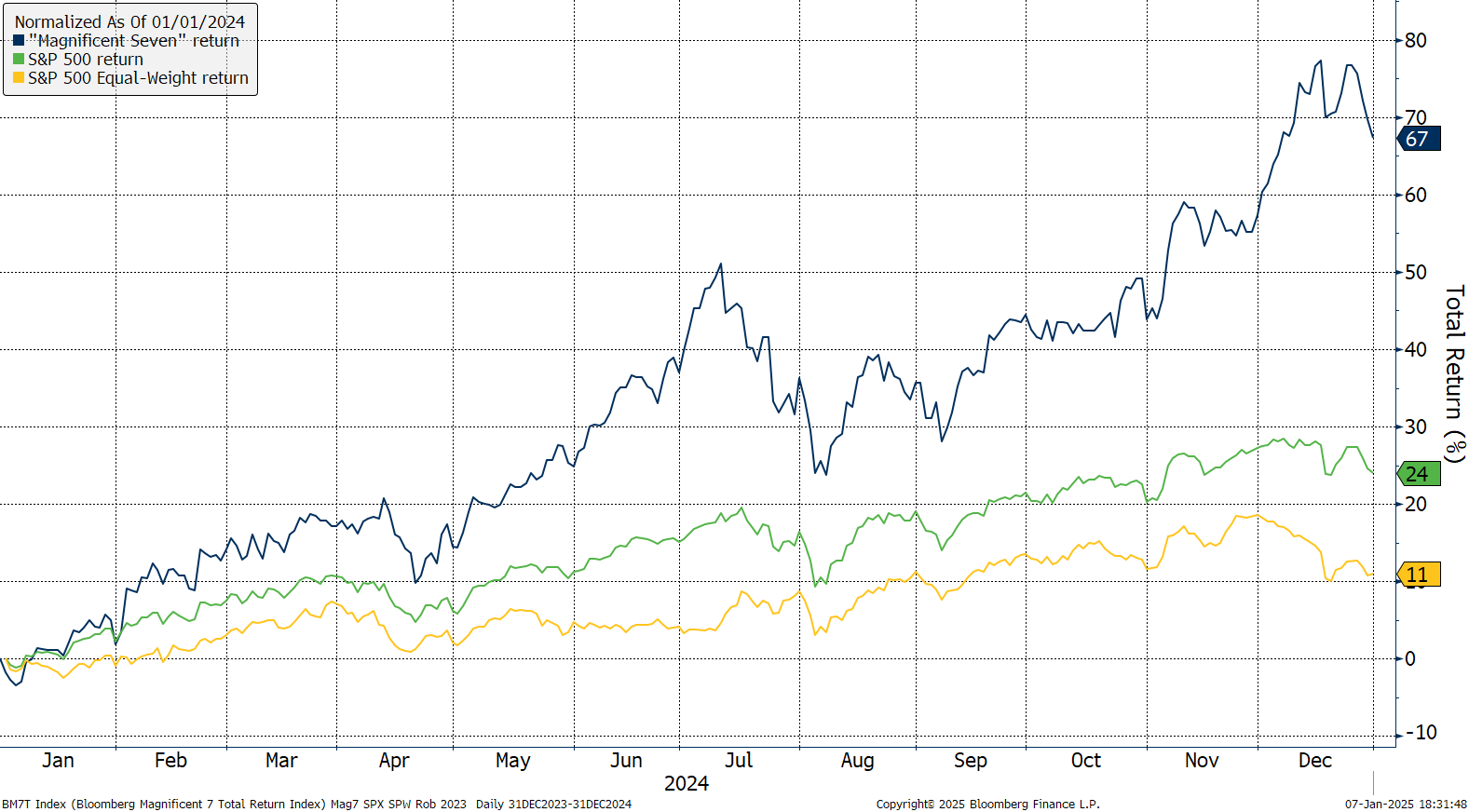

Ultimately, the US stock market delivered exceptional returns in 2024 – as it did in 2023 – again defying initial cautionary predictions. Large-cap US Growth stocks led the way to one of the best years on record. The S&P 500 Index posted a total return of 25%, after registering a 26% return in 2023. This marked the first time the S&P 500 has gained more than 20% in consecutive years since 1997-98 and represented likely confirmation that we are now in an AI-led bull market much like the “dot-com”-led rally of the late-1990s. Although that time period ended with sharp declines in equity indices, the cumulative return between 1994-1999 was 224% (26% annually); put differently, the S&P 500 was up over 20% for each of those consecutive years. By comparison, the cumulative return from the March 2020 pandemic lows until the end of 2024 has been notably lower at 172% (23% annually), and there have been only two years of returns above 20%. Investors’ memories of the dot-com bubble loom large, but we believe the earnings supporting the current AI-led rally are much stronger than the (lack of) earnings in the late 1990s.

In 2024, diversifying US equity exposures like US mid-caps (+13.9%) and US small-caps (+8.7%) also generated solid absolute returns, though they paled in comparison to the AI-driven Magnificent 7 (+67.3%), which drove the 25% gain of the S&P 500 via those stocks’ roughly 33% weighting in the index. The S&P 500 Equal Weight Index, by comparison, rose just 12.8%. (The Magnificent 7 refers to seven stocks that have driven most of the S&P 500’s returns: Alphabet, Amazon, Apple, Meta, Microsoft, NVIDIA, and Tesla).

International equities faced headwinds from geopolitical tensions, slower economic growth (especially in China) and a strong US Dollar (+7%), resulting in weak results relative to the US. Emerging market equities gained 7.8%, while developed market equities added a paltry 4.4%. The US outperformed the rest of the world for the 13th time in 15 years.

The bond market generated lackluster returns as well, with US intermediate-term bonds returning 2.9%. Despite concerns about rising interest rates, bonds remained an attractive option for conservative investors seeking steady income. Real assets had a mixed year. Real estate struggled under the weight of higher interest rates, refinancing risks and ongoing office sector woes, and finished down 1%. Other real assets (timberland, farmland, energy infrastructure, etc.) managed to outperform the US bond market, with returns approximating 3.5%.

As we think about 2025, risks have certainly emerged – elevated equity valuations and excessively optimistic investor sentiment after back-to-back 20%-plus gains, sticky core inflation potentially exacerbated by tariffs and deportations, higher long-term interest rates on higher inflation and rising concern about US debt and deficits – our forecast is generally for more of the same, though with lower total returns and more volatility. That means pro-growth, with an overweight to US equities – including the MAG7 for AI exposure – and underweight/diversifying positions in cheaper mid-cap, small-cap, and international equities, as well as fixed income and alternatives (likely to be helpful in hedging inflation risk in traditional fixed income). Given the starting point, it’s probable we’ll need to be more tactical in 2025, as bouts of risk-off are likely to be more severe than in 2024, but we still feel equities will be the highest returning asset class going forward.

Equity Market Outlook

Despite a dip in December, the fourth quarter of 2024 added to a string of recent gains in equity markets. The S&P 500 ended the year with a total return of 25% in 2024, which followed a gain of 26% in 2023. It’s unusual to see back-to-back years with returns of this magnitude, but in this instance the steady rise in equity markets has been driven by a multitude of factors: depressed valuations following the earnings recession and spike in interest rates in 2022, steady improvement in the monetary policy outlook, broadening and accelerating profit growth, and an extraordinary investment cycle in AI infrastructure. This confluence of factors resulted in pronounced leadership by large US stocks and by the shares of the very largest US companies in particular. On the other hand, international equity significantly underperformed the US market due to weaker corporate earnings growth and rising geopolitical uncertainties. As we look ahead to 2025, we remain optimistic on equities and especially on large US equities as many of the drivers of recent equity market returns remain intact. On a shorter-term basis, we are wary of current valuations and sentiment, which have become elevated despite increased uncertainty due to a shifting monetary policy and political backdrop.

One of the key themes of 2024 was the acceleration and broadening of corporate earnings growth. At the beginning of the year, market participants had anticipated a recovery in corporate profits after a challenging 2023, and the results have largely lived up to these expectations. Earnings have not only improved for the AI-driven large-cap technology companies but have also expanded across sectors that had been lagging. The broad rally has not only been driven by improving earnings but also by favorable macroeconomic conditions, such as moderating inflation and interest rates, as well as a resilient global economy.

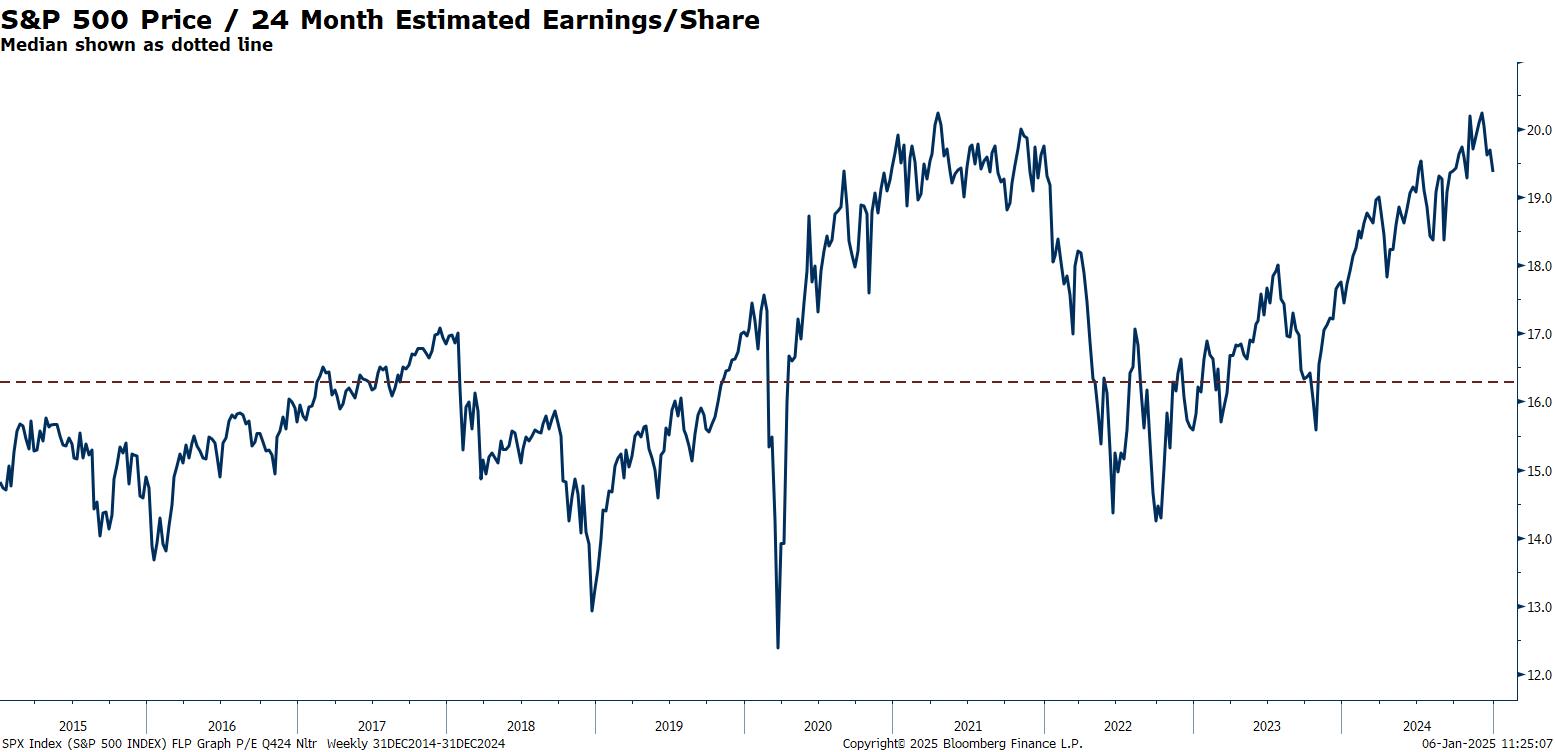

While strong earnings growth and market returns in 2024 have contributed to a favorable investment climate, they have also led to concerns about market valuations. The S&P 500, for example, is near all-time highs and boasts a 2-year estimated P/E ratio 19% higher than the 10-year median as shown below. This suggests that much of the positive outlook for future earnings has already been priced in to some extent. Equally concerning is the state of some longer-term measures of investor sentiment. After two years of remarkable equity gains, it appears that many investors have grown complacent and are taking the bullish market environment for granted. This is especially true in the more speculative corners of public equity markets such as quantum computing, which have been booming. While elevated valuations and complacency can persist for extended periods, they also create an inherent risk: if earnings growth slows or if macroeconomic factors shift unexpectedly, even modest adjustments in profit expectations could lead to a sharp correction in equity prices.

As we enter 2025, there are several key risks on the horizon that could provide a catalyst for a correction in equity markets. Political uncertainties continue to loom large, both in the US and globally. In the US, the incoming administration could introduce volatility with potential shifts in fiscal policy, taxation, and regulation. Globally, geopolitical risks could disrupt supply chains and international trade and further contribute to market instability. In addition, inflationary pressures, while moderated, are not entirely under control, and central banks may be compelled to keep interest rates higher than previously anticipated if inflation resurges. Tighter monetary policy could lead to higher borrowing costs, which would weigh on corporate profitability and potentially reduce consumer spending, both of which could have a negative impact on equity valuations.

As we look ahead to 2025, we remain optimistic about the prospects for equities for the year as a whole and over the long term, although we also acknowledge that short-term risk has increased. Valuations are stretched, and investor sentiment has become ebullient such that a correction seems not only likely but possibly imminent as shifting monetary and political factors begin to exert their influence. Investors should prepare for increased volatility, which is likely to generate attractive buying opportunities in 2025, particularly among the large US growth stocks that have been leading the market given their robust fundamentals. We remain tilted toward higher quality large US stocks over smaller or international companies and expect that taking advantage of short-term challenges by remaining focused on solid long-term fundamentals will be key to success in the year ahead.

Fixed Income

In 2024, the start of the Fed’s rate-cutting cycle and a robust US economy propelled “risk-on” sentiment within fixed income markets. In US Treasury markets, this was reflected in higher rates and a steeper yield curve, led by the 10-Year US Treasury that ended the fourth quarter at 4.57%, an increase of 0.69% in 2024. After rising as high as 5.04% in April, the 2-Year US Treasury Yield ended December at 4.24%, slightly lower than where it started the year. The realization of Federal Fund rate cuts and gradually improving inflation were the main reasons for this decrease. With a current positive spread of 0.33% between the 2-year and 10-year yields, the curve has regained a more normalized, upward sloping shape, which is a positive sign. In credit markets, positive sentiment is apparent in some of the tightest credit spreads in the last thirty years. The current high yield spread1 of +287 basis points (2.87%) is well below its 30-year median value of +435 (4.35%), reflecting minimal credit stress. Due to tighter spreads and higher rates, any fixed income sector that was lower in credit quality and short in duration performed well in 2024. Short duration Treasury Inflation-Protected Securities (TIPS) also performed admirably as inflation stalled between 2.5% and 3%, above the Fed’s stated 2% target.

Our main fixed income investment themes in 2025 are guarding against inflation, maintaining liquidity, and reducing duration. Inflation has generally been on a downward trend since early 2022, but progress has stalled over the last six months. In our view, inflation will remain problematic in 2025 with a strong labor market and wage growth leading to continued elevated levels in service and shelter inflation. We are also embarking on what is expected to be a lower tax, lower regulation, higher tariff regime under President Trump and a Republican congress, which may further increase inflation risk. TIPS remain our favored way to hedge against inflation in fixed income portfolios.

Increasing liquidity, our second theme, will be of particular focus in the year ahead if credit spreads remain tight. Spreads are at levels where even modest widening could lead corporate bonds to underperform US Treasurys. Adding liquidity enhances our ability to tactically invest when volatility inevitably overtakes markets. We continue to be selective when investing in corporate credit, focusing on bonds with attractive yields and issuers that can weather economic disruption.

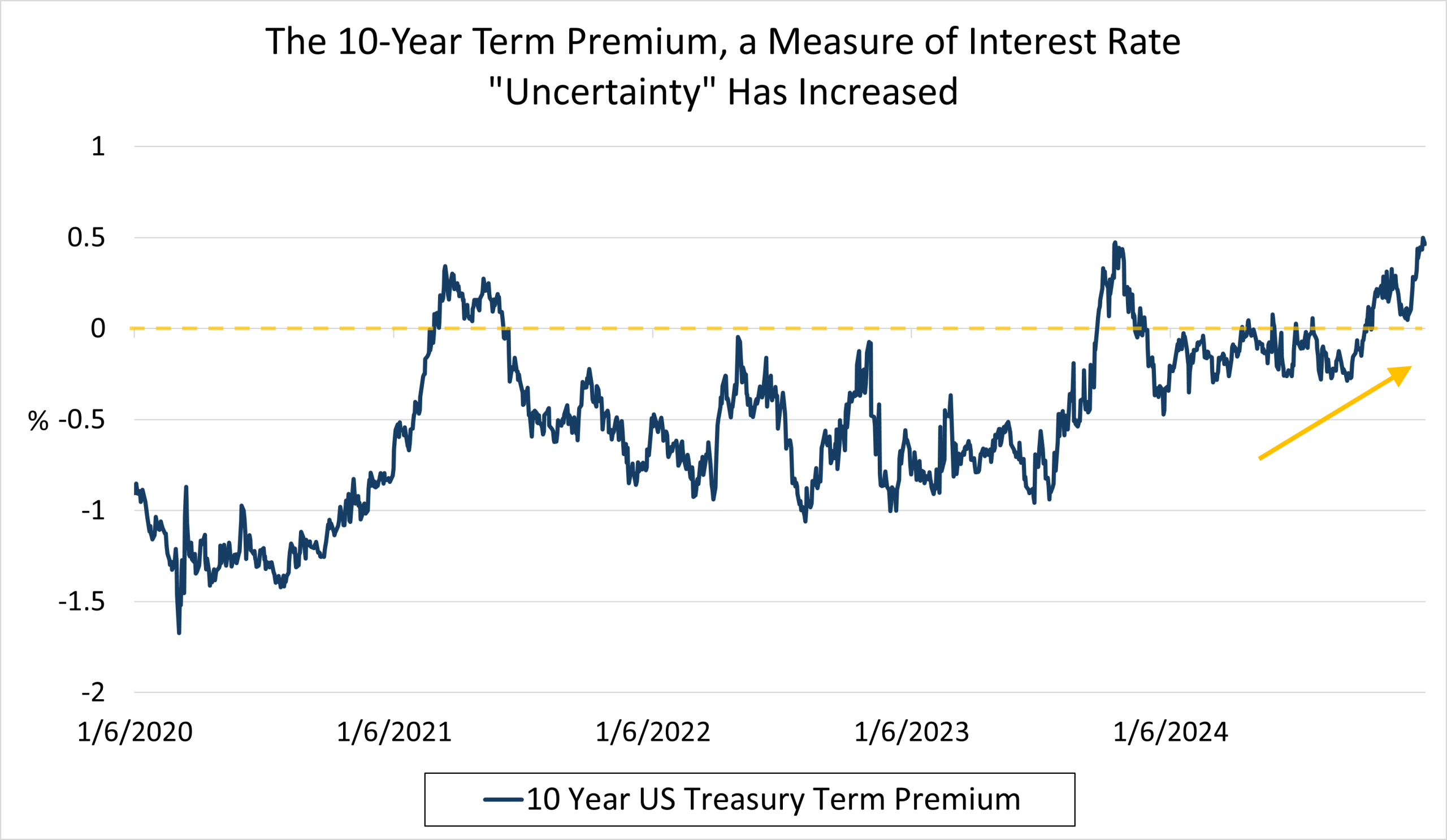

Our third theme of reducing duration is a direct response to inflation and government policy risk. Interest rate markets appear increasingly concerned about elevated deficits as evidenced by the 10-Year Treasury term premium. The term premium, which measures interest rate path “uncertainty,” has risen 75 basis points (0.75%) in the last three months. US Treasury markets remain unnerved by the prospect of runaway deficits, despite initial optimism about the newly formed Department of Government Efficiency’s plan to cut government spending by $2 trillion. After first moving lower, rates subsequently increased, as wrangling over the debt ceiling illustrated that government dysfunction is as present as ever. We plan to reduce duration slightly and remain wary of increased interest rates due to deficit concerns and policy uncertainty.

The outlook for interest rates in 2025 is cloudier than usual. Bloomberg asked fifty-one strategists where the 10-Year Treasury Yield will end in 2025, and the range of responses were as low as 2.98% and as high as 5.50%. Interest rate volatility seems inevitable as the market wrestles with fiscal and monetary policy, deficits, recession possibilities, and inflation risk. We still view corporate credit as an attractive sector in which to invest, although we are focusing on increasing liquidity within corporate credit. Municipal bonds look relatively attractive on a tax-adjusted basis, and we continue to like short-duration TIPS as a hedge against inflation. Overall, an upward sloping curve and attractive bond yields bode well for fixed income returns going forward, especially for investors who can be tactical and opportunistic in an expectedly volatile year.

Spotlight: Private Infrastructure Investments

What is private infrastructure?

Private infrastructure investing has emerged as an attractive opportunity for investors seeking exposure to both long-term global trends and stable returns. Let’s first define what infrastructure investing is.

Infrastructure investments provide debt or equity financing of physical assets that distribute resources, goods, commodities, and people across the global economy. Some examples include power grids, ports, bridges, and data centers. The essential nature of these assets across sectors including energy, transportation, and digital connectivity results in consistent demand in usage rates and, subsequently, consistent revenues. This in turn is a contributing factor to infrastructure’s lower volatility compared to other asset classes.

In addition to traditional sectors like utilities and conventional energy, the asset class includes businesses critical for long-term energy security (e.g., liquified natural gas, renewable energy generation, and circular economy businesses like energy-from-waste), the digital revolution (e.g., fiber optic networks, data centers, and telecom towers), and onshoring across industries.

Private infrastructure investments provide diversification and stability to a portfolio

Investing in infrastructure via private investments offers several advantages in a diversified portfolio. For starters, private infrastructure investments – like many private investments – exhibit low correlation to both stocks and bonds. This means when stocks and bonds zig, private infrastructure tends to zag. Second, these assets typically generate stable cash flows through long-term contracts or regulated revenue streams, often tied to inflation. This characteristic, along with the private nature of the asset class, leads to a return profile that is more stable than publicly available options like stock or real estate investment trusts (REITs). As a result of these attractive traits, private infrastructure has historically provided downside protection in down markets for stocks or bonds.

Global trends are driving infrastructure demand

With the rise of AI, rapid development of related technologies will drive demand for many critical infrastructure assets and industries. Data centers, for example, will be required to provide the infrastructure to store and transmit the growing pool of data-supporting AI tools, underscoring that AI innovations will drive increased data infrastructure.

This also dovetails into the energy equation. Just as AI creates a need for additional data storage capacity, it also materially increases energy consumption. To put this in context, recent analysis shows that a simple ChatGPT query takes three to 36 times more energy than a similar Google search. In other words, the continued adoption of AI tools will directly increase the need for additional power generation and transmission assets. This is in addition to the energy transition, where governments worldwide are incentivizing private capital to renewable energy projects, battery storage systems, and grid modernization through policies like the US Inflation Reduction Act and Europe’s Green Deal Industrial Plan.

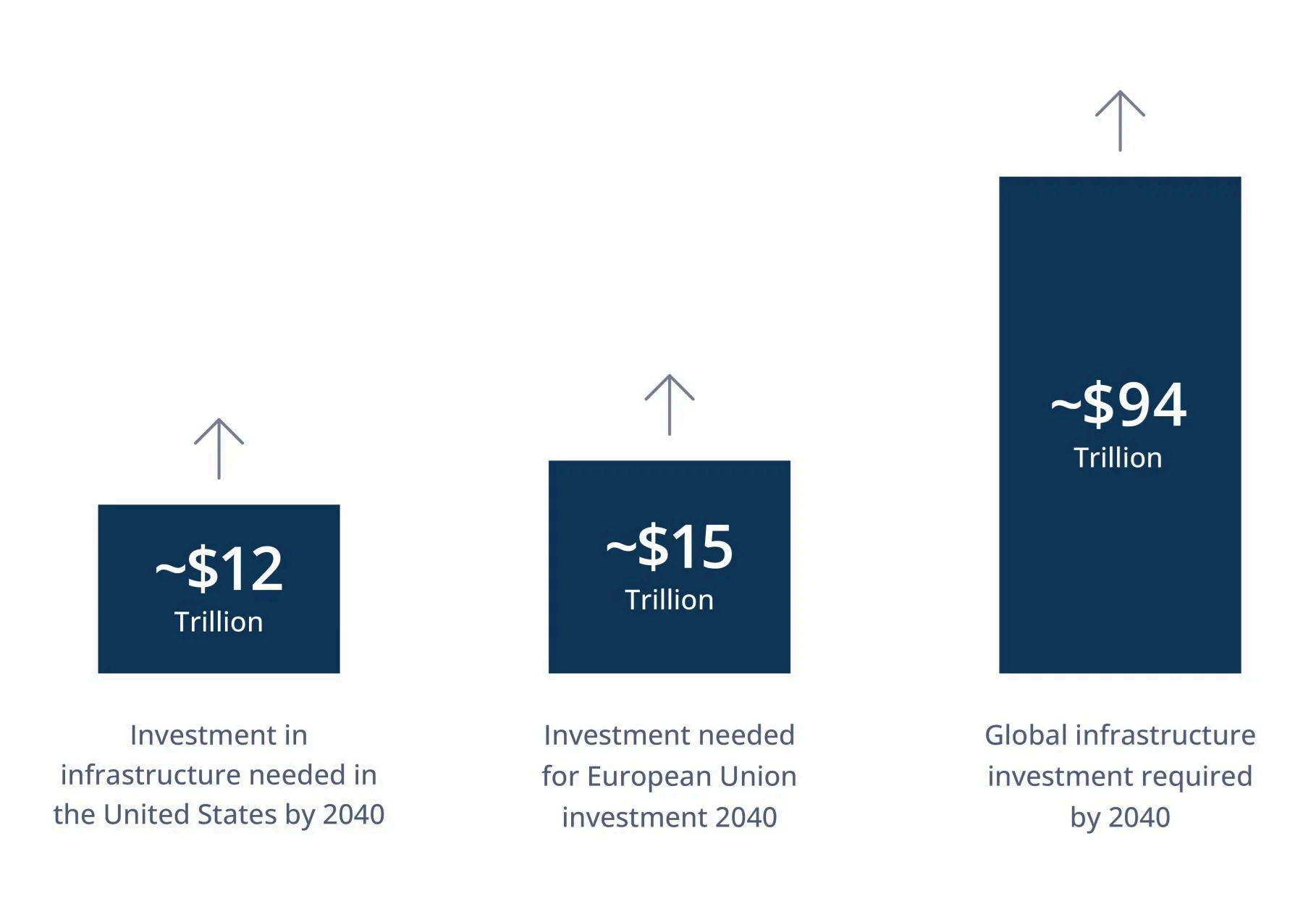

Additionally, public-sector budget constraints have widened the funding gap for infrastructure, estimated at $94 trillion by 2040 (Oxford Economics), presenting significant opportunities for private capital to address critical needs. Rebuilding the physical economy in the US—including improving and repairing infrastructure, expanding manufacturing capacity, and accelerating homebuilding—has become a topic of increasing consensus across both the public and private sectors.

Conclusion

Private infrastructure investing has emerged as an attractive opportunity for investors but does not come without risk. The most salient risk is illiquidity. The private nature of these investment opportunities is a large step away from the daily liquidity we enjoy in public equity markets. Additionally, these investments are subject to a degree of legislative/political risk. Any potential changes to the aforementioned Inflation Reduction Act by the new administration could create headwinds for certain segments of the asset class. As with all potential investment opportunities, investors should weigh rewards with risk and consider portfolio fit in their decision-making process.

Private Markets 2024 Review and 2025 Outlook

Private assets broadly appreciated in 2024 as economic growth, stable interest rates, and business confidence supported markets. Purchases and sales, captured in IPO and M&A activity, remained sluggish relative to historical standards but witnessed a pickup in the second half of 2024 that is expected to carry into 2025. Financing activity for the year was robust as private credit and public credit markets competed for a healthy refinancing pipeline, particularly once the Fed signaled dovish policy in the second half of 2024. Against this favorable backdrop, markets continued to exhibit have-and-have-not dynamics. Assets aggressively financed when interest rates were lower are struggling with the new interest rate regime, with 2018-2020 vintage real estate and private equity funds the most impacted. Owners with troubled assets are kicking the can down the road as much as possible to avoid selling or defaulting on over-leveraged assets. We expect to see more cathartic sales activity in 2025 clearing out the bad balance sheets that were put in place before 2022. Additionally, assets with substantial changes in end-market demand are being rewarded (i.e., datacenters, AI-related businesses, beneficiaries of government spending) or punished (i.e., office real estate). Investments heavily reliant on the market for additional equity investment such as cash burning venture-backed businesses or debt infusions such as cash burning private equity and real estate will continue to struggle under current conditions.

Private Equity

Overall, valuations trended positively for private equity during the fourth quarter and over the second half of 2024. For the second half of the year, private equity deal activity and distributions remained low relative to historical standards despite an uptick in activity relative to the start of the year. Against this backdrop of low deal volumes and distributions back to limited partners (LPs), fundraising remains challenging. While these trends will persist into 2025, a slow but gradual thaw is underway.

- Deal Volume/Fundraising: Capital raising rebounded in late 2024 after a slow first half, tracking to match 2023 levels despite distribution constraints. The median time to close US private equity funds stretched to 16.7 months by November 2024, up from 10.9 months in 2022 and the longest period since 2010. While dry powder exceeded $1 trillion in 2022 as fundraising outpaced deployments, this trend has reversed sharply as fundraising stalled. In 2024, most funds fell short of their target sizes, forcing them to either extend fundraising or close below target. This environment has created opportunities in seasoned primaries – funds that already contain mature investments at final close, offering reduced blind pool risk and potential immediate performance gains.

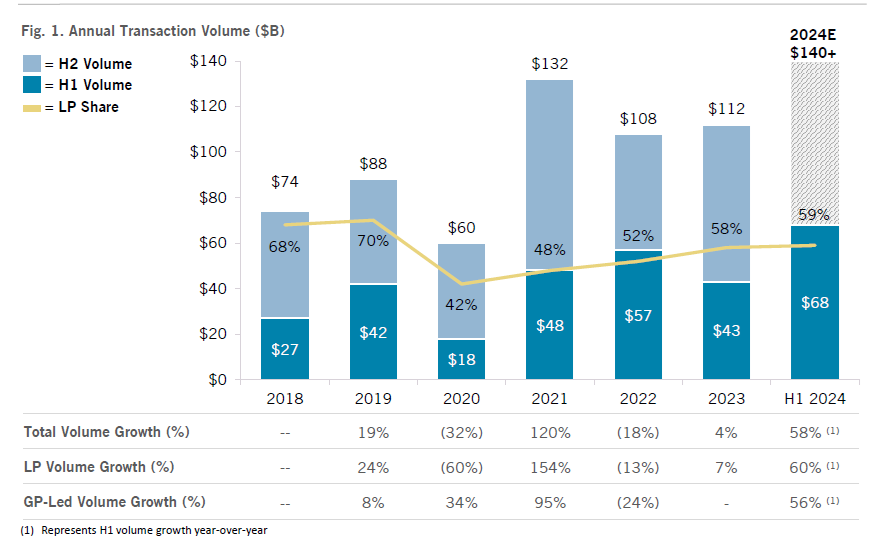

- Secondaries Activity: Secondaries activity remained robust over the second half of 2024, as managers had to be more proactive to generate distributions given sluggish M&A and IPO markets. Secondary market volumes soared in 2024, reaching $140 billion – a 20% jump from 2023 (see table below from Jefferies highlighting total global secondaries market annual transaction volume). A looming maturity wall faces private equity managers, with over 50% of active fund capital now six years or older, requiring imminent exit solutions amid limited traditional exit options. We continue to believe that GP-led secondaries are a means to obtain high-quality private equity exposure and believe the trend has many more years to go before investor liquidity issues are adequately resolved.

Total Annual Global Secondary Transaction Volume as of July 31st, 2024

Private Credit

Private Credit continued to grab headlines and be the primary allocation for investors ramping their allocations to private markets. The asset class, which was a niche market a decade ago, has now become a staple of the corporate lending sector, growing to an estimated $1.5 trillion. The past year saw strong capital raising and deal flow/issuance. With private equity deal flow muted, strong inflows into private credit led to high competition and spread compression, with most of the activity coming from refinancings of existing loans. According to Pitchbook, by 9/30/2024, refinancing deals surpassed 2023 levels, with 158 transactions versus 118 transactions, respectively. The private credit market also saw increased competition from the broadly syndicated market. Collateralized Loan Obligation formation in 2024 drove aggressive loan pricing, with 41% of deals priced at the Secured Overnight Financing Rate +500-549 bps in H2 2024, up from 7% in H2 2023, making it difficult for private lenders to compete. This suggests a normalization for performance in the 2024 vintage. The key driver for private credit opportunities in 2025 will depend on private equity deal volume recovery. Given the competitiveness in corporate direct lending, we expect market participants to diversify into asset-backed lending, infrastructure debt/equity, and real estate debt/equity to generate incremental yield.

Legacy private credit portfolios, particularly 2018-2021 vintage loans nearing maturity, reveal distinct performance patterns: strong early returns followed by credit stress in years 4-6 as weak borrowers struggle to refinance. Managers have continued kicking the can down the road on underperforming credits, notably by converting cash-pay interest to payment-in-kind interest (non-cash). This can-kicking has also taken the form of “creditor-on-creditor violence” or liability management exercises, where existing creditors take advantage of weak credit documents to create new loans and/or shift assets at the expense of existing creditors. While this doesn’t manifest itself as a loss today, upon an event of default there are the haves (credits with strong asset protection experience low losses/high recoveries) and have-nots (credits with weak asset protection experience high losses/low recoveries). To date, many managers have not appropriately written down positions for apparent credit degradation. We believe the core issue is that performance for legacy pools of private credit capital is weakening, and there should be more significant dispersion across these pools than investors are anticipating, particularly as defaults pick up in 2025 and beyond.

Real Estate

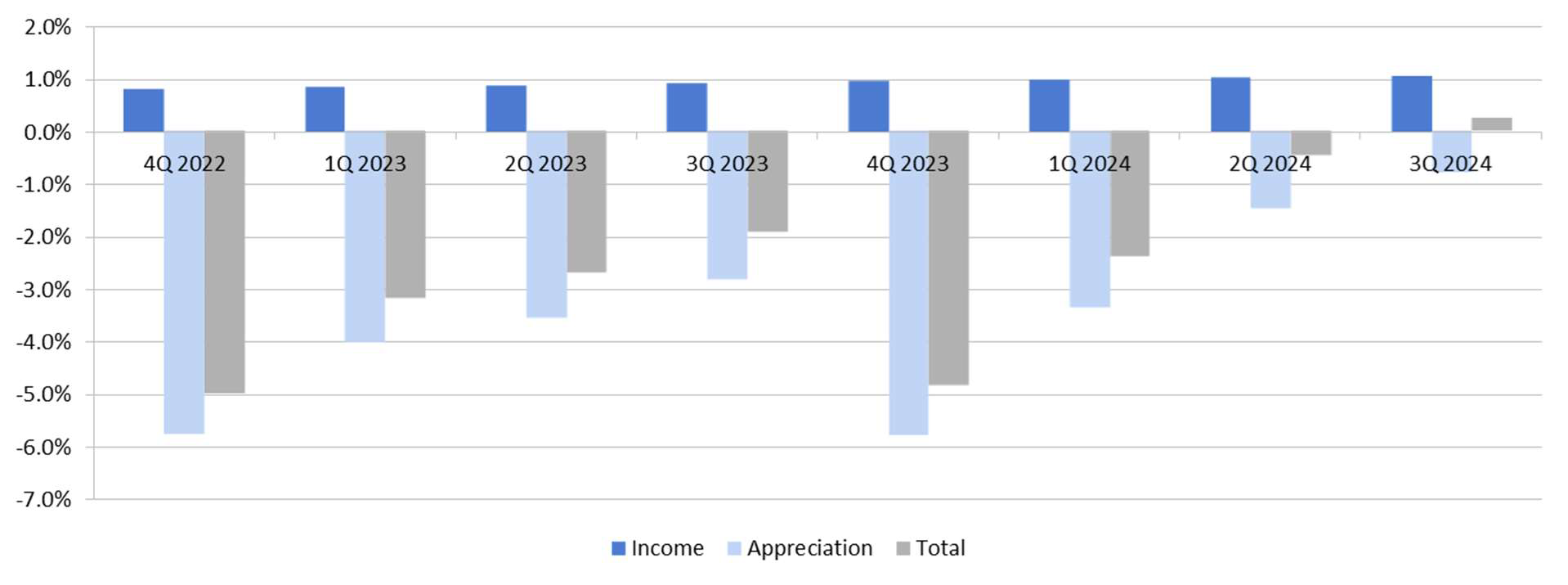

While publicly listed real estate valuations rebounded from their trough in 2023, private real estate marks continued to decline up until the third quarter of 2024, suggesting a possible inflection point particularly with respect to interest rate-related cap rate adjustments. The chart below depicts the quarterly returns for the NCREIF Fund Index – Open-end Diversified Core Equity (NFI-ODCE), which tracks the largest private real estate funds. The index generated a gross total return of +0.25% in the third quarter of 2024, its first positive quarter after seven consecutive quarters with negative total returns. It is worth noting that income during this challenging period has been consistent, with almost all the negative return based on changes in the assessed value of the underlying properties.

Core Real Estate Fund Index Total Returns Turn Positive for the First Time Since 3Q 2022

All sectors except office showed positive trends in the latter half of 2024, with office markets continuing to face disrupted fundamentals. Multifamily new construction starts have decreased by about 40% from 2022 peak levels, likely leading to lower vacancies and supporting a reacceleration of rent growth. We remain optimistic about multifamily real estate, as the persistent US housing shortage is expected to be met with strong demand. Industrial real estate continued to see strong demand given e-commerce trends and datacenters witnessed substantial euphoria over the year. Both trends seem likely to persist to 2025 and beyond, but there are growing concerns that datacenter valuations may be getting stretched, particularly for properties built on spec (those that haven’t pre-sold their capacity).

Real Assets

Real Assets are a broad asset class encompassing all types of assets (e.g. transportation equipment, power generation infrastructure, electric infrastructure, commodity pipelines, farmland, timberland), many with varied demand drivers. That said, real assets generally performed well throughout 2024. With steady economic growth, inflation above the historical average, and interest rates declining, the macroeconomic backdrop for real assets has been largely positive. These assets tend to be supported by positive economic conditions in the US, strong global trade (particularly exports) and energy demand, and sponsors have been increasing lease rates aggressively and pushing out contract lengths to take advantage of favorable conditions. Energy demand was a notable theme as investors seek secondary and tertiary exposures to the explosive growth in data centers and their associated energy needs. Although power and digital infrastructure assets have performed resiliently, they have seen significant increases to their valuations, which could likely cause future performance to normalize.

Sustainable Investing

As we head into 2025 and a new administration in Washington, the levels of concern, and even fear, are elevated across the sustainability ecosystem. There is no doubt that the operating environment will change, and perhaps materially in certain areas. While some of this concern is certainly valid, it’s important to take a step back, consider the momentum in place and keep focused on the long term.

It is reasonable to expect that pressure on corporations to dial back ESG and DEI initiatives will continue and perhaps become more pronounced in the near term. Many companies have already changed the way they characterize these programs, and more are likely to do so, though in the background, the work continues. This work will be communicated using different language and will likely be more tied to tangible business outcomes such as talent retention or resource efficiency. Larger companies will have to continue to navigate European and other regional sustainability reporting directives, so few will dial back the underlying efforts to measure and manage sustainability risks.

It is also reasonable to expect that there will be turnover at both federal and state levels in the US in early 2025, with leadership and staff-level changes. Environmental and social agendas may well be de-emphasized, and existing regulations may be targeted for rollback. Existing legislation supporting the energy transition will likely be targeted to some extent. The new administration’s desire to foster continued economic momentum and offset legal challenges will make major degradation of government programs and support challenging to accomplish.

Within the investment and capital markets industry, the marketing of products with sustainability labels has changed and the way firms communicate with clients around sustainability integration and outcomes will continue to evolve. As we’ve written previously, these changes are healthy and in the best interest of underlying clients as transparency and comparability improve. The teams of people at financial firms focused on various aspects of sustainability will continue to do their work, though like in the corporate sector, materiality and tangible outcomes will be increasingly important.

For investors specifically, the underlying sustainable investment (SI) approaches employed on behalf of clients will in some cases require adjustment, while others will continue to be largely unaffected. As we’ve written previously, each of the underlying approaches (outlined below) have different risk/return profiles and different key metrics used for implementation.

| SRI Values/mission-driven exclusion of specific investments or exposures from an opportunity set ESG Peer-relative material environmental, social, and governance risk assessment and analysis Thematic Evaluation of trends shaping a changing world that enable opportunities for growth Impact Investments intended to have direct and measurable environmental or social impact as a primary objective |

Exclusionary SRI and risk-focused ESG approaches, while quite different, are both likely to be largely unaffected. Any specific values or mission-oriented SRI exclusions are client-directed at the securities or fund level; thus, any changes would be client-driven. ESG risk management responsibility sits with the investment manager and should continue as an integrated part of a sound investment process. As noted above, disclosure of ESG information by large companies should continue, though as always, investors will need to continually assess shifting areas of risk. One recent example involves an auto and battery manufacturer that has rapidly growing water needs for a large new facility in a water-stressed region. Uncovering risks such as this and assessing related financial implications will only become more important in a higher growth, lighter regulatory touch environment.

More material adjustments and tactics will be required across thematic and impact approaches. It is in these areas where environmental regulations, supportive federal legislation, and the flow of international trade are all potentially at risk and could lead to material negative or positive impacts on companies focused on clean technology and the energy transition.

The clean-tech industry will be confronted with a number of risks. Tariff proposals outlined by President-elect Trump may create significant supply chain problems for companies sourcing raw materials in China, with solar and battery materials being two prime examples. Not only could tariffs lead to supply disruptions and higher component prices, but more broadly could drive higher levels of inflation throughout the US economy, forcing the Fed to raise interest rates. Higher interest rates would have a dampening effect on project economics across the clean-tech landscape.

Deregulation is another clear area of focus for Trump, with environmental and energy regulations squarely in the crosshairs. Based on analysis from investment bank Jefferies and agency cost estimates, EPA and energy-related regulations put in place under the Biden/Harris administration are expected to cost businesses and the economy roughly $1.3 trillion over ten years, despite accompanying environmental benefits. Vehicle emissions and greenhouse gas standards represent roughly three-fourths of the total estimated costs, so will likely be early targets. Deregulatory efforts, if enacted, would likely reduce incentives for companies to invest in environmental protection, reduce pressure to invest in cleaner products, and potentially lead to lower traditional energy prices, thus weakening the relative positioning of higher cost cleaner products.

Attacks on recent energy transition legislation such as the Inflation Reduction Act (IRA) are also top of mind for clean-tech companies and investors. Any material extension of tax cuts enacted in Trump’s first term will require cuts elsewhere, with the IRA a prime target. As we’ve discussed in the past, the IRA was the most significant piece of climate legislation ever signed and our only real chance to stay within Paris Accord climate targets. President-elect Trump’s negative sentiment toward electric vehicles and clean energy along with the cost of the IRA make the possibility of changes here likely, with consumer electric vehicle purchase credits most at risk.

While the road ahead for clean-tech sounds challenging, there are still many positive drivers that should provide some counterbalance to the risks noted above, and in some cases may result in improved outlooks for certain companies.

Efforts to roll back environmental and energy regulations will meet resistance through legal challenges from states, NGOs, and others interested in maintaining environmental protections, meaning any progress on deregulation will be difficult to achieve. On the other hand, when it comes to regulatory reforms, there are areas of bipartisan agreement, such as power transmission and interconnection. According to Bloomberg New Energy Finance, roughly three times the existing total installed capacity of renewable energy and storage is waiting for grid connection in the US. Reform here could bring renewable power to market more quickly.

Wholesale repeal of the IRA appears unlikely as more than 80% of funding to date supports fixed asset investment in states where Republicans won elections in November. States where economic growth and job creation are occurring will seek to protect these gains. There was evidence of this in August when 18 Republican House reps wrote to Speaker Johnson in support of IRA energy and manufacturing credits. It’s also clear that there is bipartisan agreement that a US manufacturing renaissance should be supported to create jobs and reduce dependence on China.

Perhaps most importantly, the underlying economics and availability of clean technologies are increasingly attractive. Solar, wind, batteries, and other components are at scale and costs—which continue to decline—are attractive relative to other forms of energy and propulsion in many markets. A read through the annual Lazard Levelized Cost of Energy report makes this point clear. Beyond attractive cost profiles, these technologies are available for deployment, whereas building a new natural gas-fired power plant would take many years given construction time and equipment backlogs. Power demand is rising now as discussed last quarter, and the companies driving this demand have serious and ambitious decarbonization targets that are well-established and unlikely to be rolled back.

Tying all this together for the IRA, we believe electric vehicle purchase credits are likely to be quickly phased out, offshore wind will likely be held up by more stringent permitting, while production and investment tax credits for other forms of clean energy and storage may well revert to a phased step-down schedule similar to what existed before the IRA. Other provisions related to supply chain manufacturing, critical materials, nuclear, hydrogen, carbon capture, and other areas are likely to remain in place.

Within our proprietary sustainable thematic investment strategies, we have deemphasized electrified transportation and most renewable energy exposure, while selectively emphasizing exposure to companies focused on clean water, sustainable food, energy efficiency, the circular economy, and nuclear power. As noted in our coverage of natural capital last year, environmental thematic investing is quite broad, enabling flexibility to manage risk in a dynamic environment.

This same research and positioning informs our ongoing evaluation of outside managers with strategies centered on private thematic and impact investments.

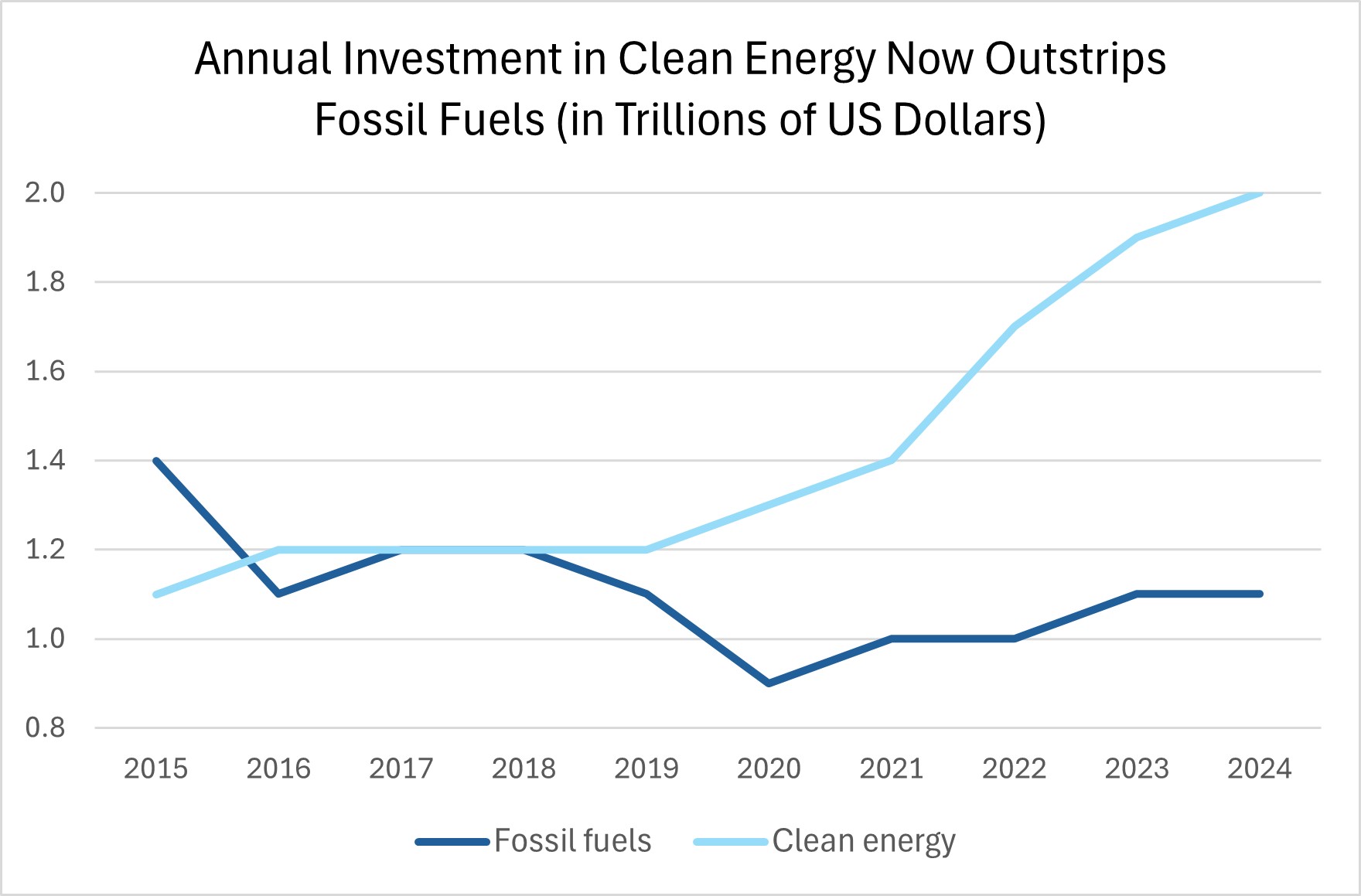

We and so many others will continue to do the work that matters, evaluate ESG risks, seek thematic opportunities, and direct capital to areas of impact. Sustainability professionals in other industries will continue to do their work. There is a level of scale and momentum that has been built over many years, with costs falling, volumes rising, and capital being invested. Nowhere is this more evident than in energy transition investment, where clean energy investment is now well above investment in fossil fuels based on IEA data.

The transition to a more sustainable future will continue because it has to and because all of the people passionate about change will not stop moving forward with a focus on what is important in the long run.