The first quarter of 2026 will be remembered in a single word: Iran. What began as a year of constructive rotation and broadening stock market leadership ended in geopolitical shock, with US-Israeli military strikes on Iran in late February igniting a regional war, closing the Strait of Hormuz, and triggering what the International Energy Agency (IEA) called the largest oil supply disruption in the history of the global energy market.

Read on for in-depth discussions of the equity, fixed income, and international markets, as well as what’s going on with shifting energy policy and private credit fears.

Macroeconomic Overview

Coming into 2026, market foundations were solid. The US economy and corporate fundamentals were strong, with consensus expectations calling for over 15% earnings growth for the year. A healthy rotation was already underway – away from the Magnificent Seven and into value, small caps, and real assets – reflecting a broadening of the bull market rather than its end. Then the war changed everything.

As a result, the broad stock market fell in Q1, led by technology and communication services, while value, small caps, and dividend payers held up. The S&P 500 Index lost 4.4%, its worst quarter since Q3 2022, but that headline masks important dispersion. Q1 was especially painful for US large-cap growth stocks. The Russell 1000 Growth Index fell 9.9%, its fifth-worst quarter versus the Russell 1000 Value since data began in 1979, according to Ned Davis Research. Meanwhile, the S&P MidCap 400 Index eked out a 2.5% gain, paced by AI infrastructure plays, while the S&P SmallCap 600 Index rose 3.6%.

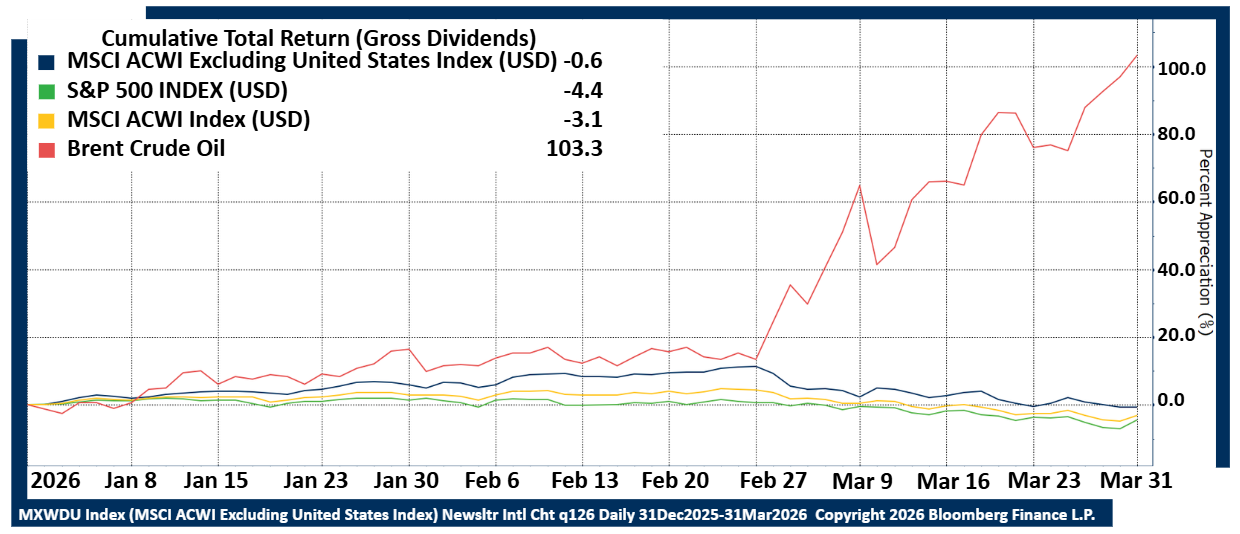

Internationally, the story was complicated. International stocks began the year with their best relative performance vs. the US since 1988 but then dropped 13% (MSCI World ex-US) to 14% (MSCI Emerging Markets) peak-to-trough in the weeks following the war’s outbreak – versus a roughly 8% decline for the S&P 500. By quarter end, however, both developed and emerging market stocks still outperformed domestic large caps for the quarter, though the margin narrowed sharply. The MSCI World ex-US Index finished down 0.8% in dollar terms, while the MSCI EM Index finished down just 0.1%.

The bond market delivered its own shock. Rather than declining on safe-haven demand, the 10-Year US Treasury yield climbed from 3.96% at the end of February to as high as 4.26% in the first week of fighting. By late March, the 10-Year yield hit 4.48%, its highest since July 2025, sending mortgage rates to near 6.5%. Investors priced in no Fed rate cuts for 2026, with the dollar emerging as the true safe-haven, rising 2.4% on the month. Intermediate bonds held up better than long duration, and we continue to favor intermediate-term maturities and higher-rated bonds amid the uncertainty.

AI remained a powerful undercurrent, though its market expression shifted dramatically.

Software stocks saw particularly severe drawdowns from all-time highs – several major companies’ stocks fell 30% to 60% – as increasingly capable AI agents led investors to sour on Software-as-a-Service (SaaS) business models. The investment in AI infrastructure continued, however, with mid-cap AI infrastructure plays in memory and networking soaring. Emerging markets, too, remain a significant beneficiary of this trend, given their dominant positions in advanced chip and memory manufacturing across Asia.

Thus far, losses to balanced portfolios have been relatively small and our base-case remains that markets recover on steady economic growth, limited long-term inflation impact, and eventual policy easing. S&P 500 earnings are still expected to grow roughly 13% in Q1, which would mark a sixth consecutive quarter of double-digit gains.

But the risks are real and somewhat binary. The Treasury market sits on a knife’s edge, torn between near-term inflation fears and the risk of economic deceleration later in the year. The European Central Bank (ECB) has already warned that a prolonged conflict could push Germany and Italy into recession. The UK’s inflation is expected to breach 5%. A stagflation scenario – sticky inflation plus slowing growth – would be a problem for both equities and bonds simultaneously.

Historically, markets have recovered from every major conflict like this. Further, NDR data on the several months preceding mid-term elections shows that equity drawdowns of this type have frequently resolved into strong subsequent returns, though with a wide range of outcomes and a small sample size that warrants humility. The mid-term election cycle itself adds a political variable: in eight months, the composition of Congress will be redetermined. A changed legislative landscape could reshape fiscal policy, defense spending priorities, and the regulatory backdrop for AI, all of which feed directly into market multiples.

This episode is consistent with previous critical junctures, which can obviously break in either direction. The economic foundation remains intact – if the Iran conflict ends soon. If it doesn’t, elevated oil prices, reignited inflation, and a sentiment shock to consumers and businesses create the conditions for something worse: the thing that derails the long bull market and begins a painful multi-year bear. Rest assured we are watching closely and are prepared to adjust portfolio exposures to reflect the realities on the ground.

US Equity

We began the year cautiously optimistic on prospects for US equities in 2026 given the combination of loosening fiscal and monetary constraints and continued investment in AI infrastructure. We had also noted that some combination of a softening labor market, lingering inflation pressures, and ongoing political and geopolitical uncertainty were likely to create some volatility along the way. Three months later the conflict in Iran has made all of these risk factors meaningful headwinds for financial markets and economic growth. Our overall assessment of equity markets, however, remains cautiously optimistic as earnings estimates have continued to rise, although the range of potential outcomes has increased.

The conflict in Iran has caused a surge in energy prices that could slow economic activity and increase inflation to an extent that could overwhelm economic support from loosening monetary and fiscal policy constraints. As these growth drivers have been called into question, estimated earnings for the year have begun to shift. Industrial and Consumer Discretionary sector earnings are the most exposed to energy price risk and have seen the worst earnings revisions over the past 3 months. The estimated 2026 earnings of these sectors are down a little less than 2% over the past three months, although they are still expected to grow 6-7% over the course of the year.

While certain companies, industries, and sectors have been negatively impacted by rising energy prices, resurgent energy prices have been a boon to the energy and materials sectors, which have seen earnings estimates revised higher by 20% and 7%, respectively. Combined with another spike in earnings estimates for the tech sector of almost 12%, sectors with substantially rising earnings estimates have more than offset marginally softening estimates in economically sensitive areas. Estimated 2026 S&P 500 earnings have increased over 4% so far this year and are now expected to grow 16% over 2025 earnings.

Tech sector profitability remains an important factor for the US equity market outlook as the investment cycle in AI infrastructure continues to outpace rapidly rising expectations. Under the surface however, there has been a notable shift in the composition of the sector’s earnings. Companies with the largest capital expenditures related to AI infrastructure have begun to face heightened scrutiny, with the market responding particularly negatively to recent reports that these investments may temporarily eliminate free cash flow for some of the largest tech companies. For the moment, the immediate revenue recognition of AI hardware suppliers is outpacing the depreciation of the AI investments and driving earnings estimates for the sector and market higher. This tide will eventually turn, but tech-sector earnings are an important support for the stock market for now.

In addition to questioning the return on AI infrastructure investment, markets have begun to discount potential winners and losers from AI disruption. AI has caused the value of software and service solutions for everything from transportation and logistics to insurance brokerage to be called into question, but these changes are not yet reflected in estimated earnings. Many of the businesses under assault by newly emerging AI-enabled competitors operate under long-term contracts, and the erosion of earnings power is likely to be a long-term rather than short-term problem. Some of the lost earnings potential in these areas is also likely to be offset by increased earnings in areas that can use AI to cut costs and increase productivity.

While long-term uncertainties continue to simmer, estimated earnings for 2026 have shifted higher while equity markets have dropped. This has resulted in S&P 500 valuations dropping to last year’s lows as shown in the chart below of the estimated Price/Earnings Ratio (a common valuation measure of how much an investor pays per dollar of estimated corporate profits). This shift in valuations could be an opportunity for long-term investors, but much depends on the path of energy prices from here. If the Iran conflict is wrapped up in a matter of weeks, most economists expect the impact on corporate earnings to be relatively modest and short-lived. In that case, prior trends could reassert themselves and corporate earnings growth in 2026 could expand beyond the technology sector that has been driving earnings growth. This would be a welcome development for a market that has become concentrated following years of narrow market leadership and robust equity returns. If instead the war in Iran rages on for months, increased volatility from economic uncertainty is likely to be compounded by policy uncertainty as mid-term elections approach this fall. While we are mindful of the risks involved, valuations provide some comfort and we remain cautiously optimistic on earnings growth and US equities as a result – especially higher quality areas that can thrive in an uncertain environment.

International Equity

Global equity markets entered 2026 on firm footing, supported by resilient earnings growth and worldwide ongoing AI investment enthusiasm. However, the eruption of the US-Israel-Iran conflict on February 28 sent Brent crude surging above $118 per barrel (up 103% in Q1), reintroducing stagflation risk into the global economy. After three consecutive years of gains and record-breaking resilience, global equities hit a wall in Q1 2026, with the MSCI World Index falling 3.5% for the quarter. Despite the headwind of a stronger US dollar (appreciated 1%), international equities again provided meaningful diversification benefits, with the MSCI ACWI ex-US Index returning −0.6% versus a -4.4% for the S&P 500.

Developed international markets retreated after four consecutive quarterly gains, with the MSCI EAFE declining 1.1%. Europe was the weakest region within developed international markets, reflecting the region’s heavy reliance on both Middle Eastern oil and liquefied natural gas (LNG) imports. Eurozone equities fell 4.2% as ECB policymakers revised 2026 GDP growth lower by 0.3%. German equities were particularly weak, dropping 8.4% due to the country’s energy-intensive manufacturing base and intensifying competition from China, while French equities fell 5.4% amid ongoing political uncertainty and fiscal constraints. However, UK equities rallied by 2.0%, benefiting from higher exposure to commodity-linked and defensive sectors. Japanese equities remained a relative bright spot, gaining 1.5% in the quarter. Expansionary fiscal policy under Prime Minister Takaichi, negative real interest rates, and ongoing corporate governance reforms continued to support investor confidence and capital inflows.

Emerging markets (EM) were roughly flat in Q1, with the MSCI EM Index returning −0.1%, outperforming both developed international and US equity markets again. The divergence within EM, however, was striking. Korea and Taiwan surged 16.7% and 9.1% respectively, benefiting from their strategic role in the global semiconductor supply chain. Peru and Brazil rallied 20.8% and 19.2%, driven by higher oil and commodity prices. By contrast, India continued to underperform the rest of EM, declining 18.1%, undermined by heavy dependence on energy imports and fallout from US tariff and visa restrictions. China fell 8.9% as the oil shock compounded already sluggish domestic demand.

Looking ahead to Q2 2026, we maintain a constructive view on international equities, though with a more cautious near-term stance. International equities still trade at a 28% discount to US peers and are expected to deliver 17.5% earnings growth in 2026. The key variables are the duration of the Iran conflict and the path of oil prices. A relatively quick de-escalation could support a meaningful rebound, while a prolonged conflict would likely weigh further on both sentiment and earnings. Even so, Europe’s medium-term growth thesis remains intact, anchored by ramping defense spending, Germany’s upcoming fiscal stimulus, and a broader re-industrialization push. We remain constructive on Japan given its pro-growth fiscal stance and improving earnings fundamentals. Within EM, we continue to favor Korea and Taiwan as prime beneficiaries of global AI infrastructure investment, while remaining cautious on India and China. We maintain a quality-focused, bottom-up stock selection approach, emphasizing companies with pricing power and energy-resilient business models to navigate likely elevated volatility ahead.

Fixed Income

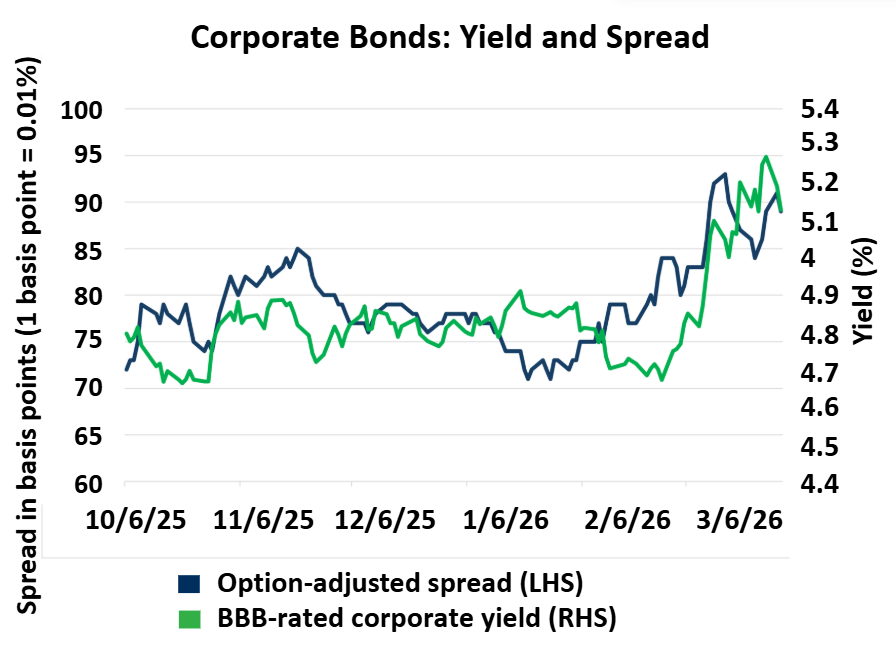

In our yearly outlook, we touched on three fixed income themes that guide our current investment decisions: staying short duration because of the potential for rising rates, maintaining inflation protection, and carefully diversifying credit exposure. We also cautioned that we expected volatility, albeit with uncertain timing and cause. Only three months have elapsed in 2026, but the military operation in Iran is an early source of volatility that reinforces our fixed income themes. Since the end of February, the price of oil has spiked by over 50%, causing interest rates and inflation expectations to sharply increase. After declining to start the quarter, the 10-Year Treasury increased by 0.40% in March to a yield of 4.32%. The 2-Year Treasury rose by a similar amount, ending the first quarter at 3.97%. Current market yields look enduring now that the market is forecasting zero interest rate cuts for the remainder of 2026. In this environment, our short-duration positioning and allocation to Treasury Inflation-Protected Securities (TIPS) have helped support portfolios. We also added an allocation to emerging market bonds to diversify credit risk and US Dollar exposure.

In the near term, Iran-related headlines and the expected duration of the conflict are driving market volatility. Even so, the underpinnings of the US economy remain strong, and we are seeing opportunities resulting from higher interest rates and wider credit spreads. Specifically, we have been buying bonds issued by high-quality companies in the 7-to-10-year maturity range, effectively locking in attractive yields for future years. These may prove especially beneficial if yields decline in the future, which could occur in at least two scenarios. If the conflict in Iran arrives at a satisfactory resolution, inflation concerns may be alleviated. Conversely, if the conflict continues, economic momentum could be derailed. While this is not a desirable outcome, it would likely lead to a decline in rates that would favor longer maturity bonds. Currently, the evidence on the ground from company commentaries suggests a stable US economic outlook, but we are closely watching for evidence to the contrary.

The Iran conflict is a current source of volatility, but it will likely not be the last in 2026. Mid-term elections, the transition to a new Fed chairman in May, private credit jitters, and an ever-shifting outlook for AI are all prime candidates to disrupt markets. Accordingly, we are focusing on building resilient fixed income portfolios that will perform in a variety of market conditions. Within the corporate and municipal sectors, that means buying high-quality issuers with strong balance sheets and stable cash flows. Within the corporate market specifically, we are also wary of companies that could potentially be disrupted by AI. The yield and relative value in both sectors are materially higher than they have been in a few months. We are positive on both the securitized bond sector because of its collateral-backed cash flow characteristics and emerging market debt due to its yield and diversified risk profile. With market volatility leading to higher yields and wider spreads, we see this as an environment where fixed income can deliver solid returns for clients.

Energy Transition

As geopolitical tensions drive volatility across markets via the Iran conflict and its impact on supply chains, we are reminded that the traditional energy system is rooted in instability and environmental challenges. In the background, power demand is inflecting higher and the energy transition continues apace.

The leading hyperscalers developing AI infrastructure, the primary power demand driver, understand the challenges this poses to the power system and have become major investors in clean energy generation to meet their explicit climate commitments. At the same time, US policy continues to support low-to-zero carbon high-capacity power through the OBBBA, spanning energy storage, nuclear, and geothermal. This alignment of corporate demand, public policy, and technological innovation is accelerating capital investment, with geothermal emerging as a growing focus.

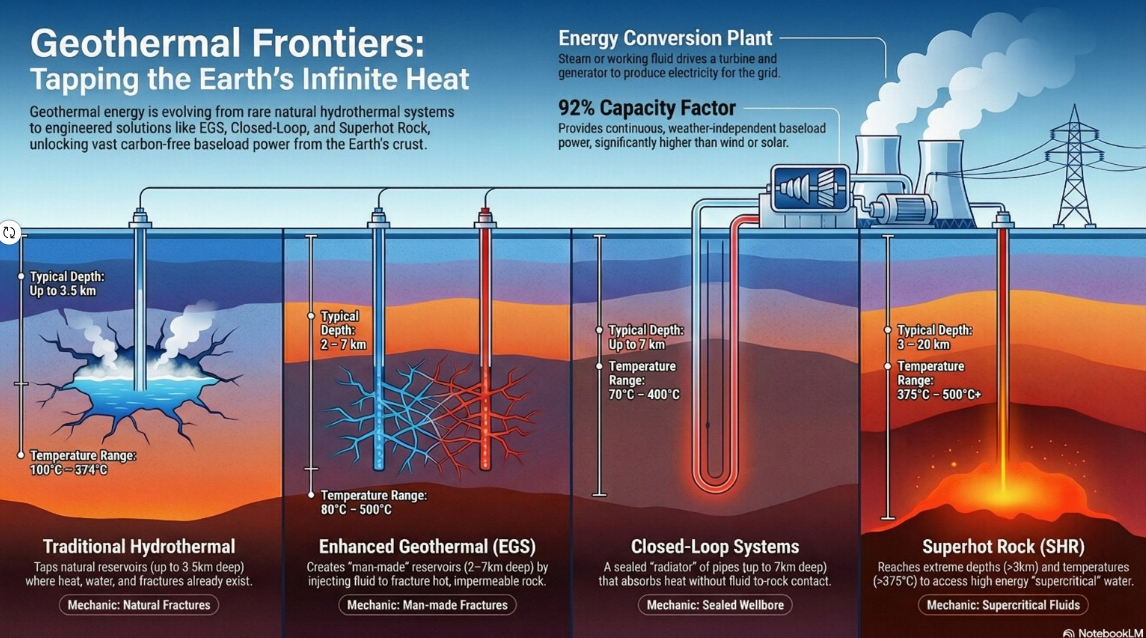

Traditional hydrothermal power relies on naturally occurring reservoirs with a specific combination of heat, water, and rock permeability. However, these specific geologic requirements have historically constrained deployment and limited scale. In recent years, several start-up companies have developed “next-generation” geothermal (NGG) technologies that use modern drilling techniques to engineer these natural characteristics. NGG has the potential to transform geothermal from a geologically constrained resource to a predictable engineered manufacturing process with vast potential.

Three NGG techniques are currently in development. Enhanced Geothermal Systems (EGS) is the most advanced technique, using horizontal drilling and fracturing to create permeability, though this comes with seismicity and water-intensity risks. Closed-Loop Systems (CLS) use directional drilling and pipes to virtually eliminate subsurface fluid interaction and seismicity risks, though heat transfer efficiency is lower and costs are higher. Superhot Rock Systems (SRS) are earlier stage but offer significantly higher energy density and a reduced footprint, despite the technical hurdles of very deep drilling.

While these techniques carry environmental risks inherited from the oil and gas industry, the industry is working to address them through microseismic monitoring, double-walled casing, and 100% reinjections. Ultimately, the geothermal industry needs to build public trust through demonstrated operational performance before scale is possible.

Scale also requires cost reduction. Currently, NREL-National Renewable Energy Laboratory, estimates that hydrothermal projects have a levelized cost of energy (LCOE) around $82/MWh, while EGS is closer to $107/MWh. Encouragingly, private developer Fervo reported a nearly 50% reduction in drilling costs at their Cape Station project. Aggressive NREL scenarios suggest EGS LCOE could reach $45/MWh by 2035, making it competitive with natural gas combined cycle projects in less than a decade. With OBBBA tax credits, geothermal could become one of the most cost-competitive forms of new power generation.

Geothermal energy also plays a unique role in grid stability. The large rotating turbines provide physical inertia that resists sudden changes in frequency and voltage, a service that is increasingly valuable as intermittent renewable energy is added to the system. Today, the US has roughly 4 GW of installed geothermal capacity, but NREL estimates this could reach 38 GW by 2035. Given capacity factors over 90%, geothermal could supply about 6% of total US electricity generation within a decade. While hydrothermal resource potential is 23 GW, NREL estimates NGG approaches like EGS have a resource potential of more than 7,400 GW.

Major technology companies are actively commercializing this technology; Google has already sourced power from an EGS project for a datacenter, and Meta has signed agreements for projects in Texas. Furthermore, the Department of Energy’s Wells of Opportunity program evaluates millions of miles of inactive oil and gas wells for geothermal recovery, which could unlock 300 GW of capacity by 2050.

Geothermal is evolving from a niche resource into a highly scalable manufacturing industry, offering the dispatchability of gas with the zero-emissions profile of solar. This convergence of heavy industry and a tech-centric future has the potential to reshape power markets and investor perceptions.

Alternative Assets

FLP is closely monitoring the recent spate of headlines highlighting concerns in private credit markets.

Over the past decade, private credit has grown into a roughly $3 trillion asset class as yield-starved investors gravitated towards the higher returns offered versus traditional fixed income investments. Where the asset class was once funded by large institutional investors (pension funds, endowments, and sovereign wealth funds), the largest alternative asset management firms have increasingly focused on private wealth management over the past few years, raising billions of dollars for “semi-liquid” funds that offer ease of access for high-net-worth investors. These funds promised periodic liquidity through quarterly redemption windows, a mechanism that offered the allure of liquidity in normal environments, but carried inherent structural vulnerabilities, namely that redemption pressure could create a “run on the bank” scenario if investors redeemed en masse. After mounting concerns over opaque valuations and deteriorating credit fundamentals, these tensions have come to a boiling point over the past several weeks. Many semi-liquid funds have seen a sharp uptick in redemptions, which have prompted managers to “gate” or limit the amount of capital available for redeeming investors.

On one hand, these issues seem entirely predictable from the standpoint of offering otherwise highly illiquid assets to less sophisticated investors through liquid fund structures. On the other hand, the degree of negative headlines and fearmongering appears to be outpacing the fundamental reality of performance for these funds. While some degree of return erosion is likely inevitable, we do not foresee fundamental credit scenarios that result in sharply negative returns across the asset class. The majority of private credit loans are used to make first-lien, senior secured loans to professionally managed, private-equity backed mid-sized businesses in the US, with loans being repaid as long as those businesses remain going concerns.

We do, however, expect redemption pressure to continue in these vehicles over the medium-term, and expect that fund managers will prudently limit outflows to wait for the underlying assets to turn to cash. It helps that credit investments naturally generate liquidity through regular principal and interest payments. For investors that are stuck waiting in a redemption queue, it appears likely to expect at least a 6- to 12-month wait for redemptions to be paid.

Perhaps most importantly, we do not see significant risk of contagion that could bleed into other financial markets. Private credit funds tend to have fairly conservative leverage, typically using less than one dollar of borrowed capital for every equity dollar of investor money in the fund. This limited use of leverage mitigates potential losses and downside risk to the asset class and makes it less likely that investors will experience losses in private credit portfolios that are funded by selling other asset classes. The prudent use of fund-level gates will allow managers to avoid scenarios in which they are forced to fire-sale assets at distressed prices. Over the long-term, we expect the fundamental credit story will win out over short-term headline noise, although we will continue to monitor this actively evolving situation.