By Ellen Hazen, CFA®, Chief Market Strategist

- Growth remains resilient despite geopolitical uncertainty

- Earnings upside is exceeding expectations and supporting equity valuations

- Markets are being driven by an expanding AI capital spending cycle

- Prediction markets can offer incremental signals

Macro backdrop. Entering 2026, we saw three positive forces underpinning the US economy. Fiscal stimulus provided both individuals and companies with lower tax rates, including the elimination of taxes on tips and overtime for individuals, and accelerated depreciation for companies. Monetary stimulus was also positive, as the Federal Reserve (Fed) had reduced the Federal Funds rate by 1.75% over the preceding 24 months, stimulating demand. Finally, capital spending on artificial intelligence (AI) has been a uniquely large and powerful stimulus. Just the four largest hyperscaler companies – Meta, Alphabet, Amazon, and Microsoft – are currently estimated to spend $700 billion in 2026 (an increase of $230 billion compared to the estimate at the beginning of the year). At roughly 2.2% of US GDP, this represents one of the largest infrastructure buildouts outside of electricity, railroads, and the internet.

AI spending as growth engine. AI capital spending has broadened beyond chip makers like NVIDIA. We are seeing accelerating revenue growth in companies ranging from industrials across power, cooling, and grid infrastructure to utilities dramatically increasing their power generation capacity to engineering firms building both data centers and power generation. Bottlenecks continue to rotate; when one is fixed, another emerges. Recent bottlenecks are CPU chips, servers, and memory chips. This strength in investment is now showing up in corporate earnings.

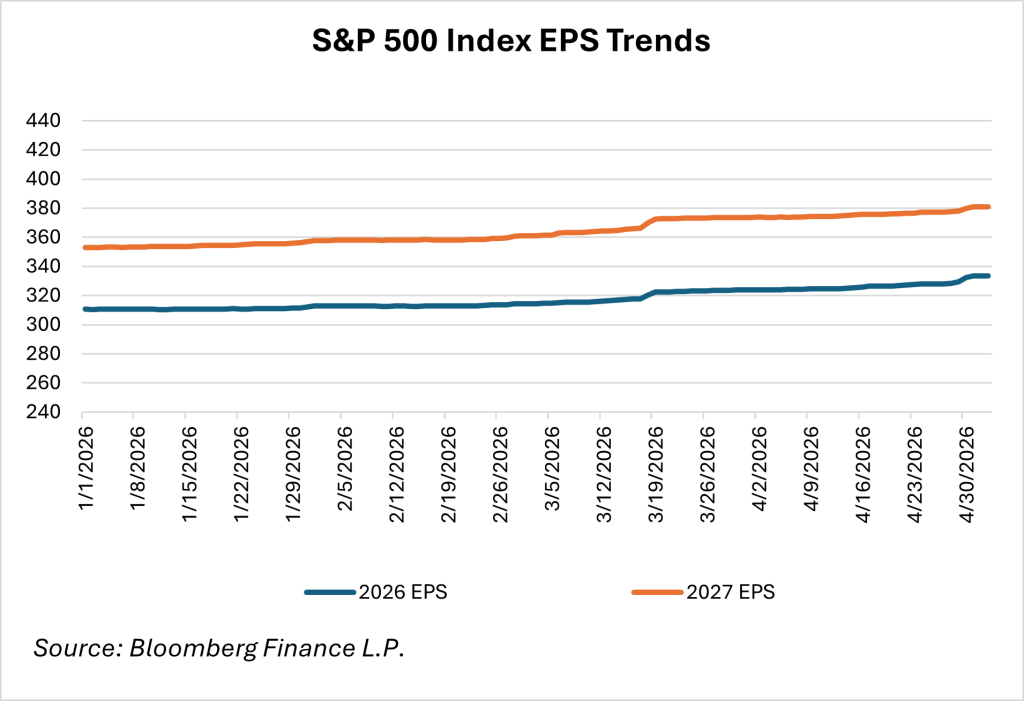

Corporate earnings are driving strong equities. Earnings growth in 2026 has likewise increased; at the beginning of 2026, consensus expected S&P 500 earnings to grow by 14%; today, that is 21%. With 75% of the S&P 500 stocks having now reported Q1 2026 earnings, we can see that growth was much better than expected; earnings grew by 19% on very strong revenue growth of 11%. After a weak performance in March, equities rebounded nicely in April, flipping year-to-date returns from negative to positive. Because earnings estimates have increased, the forward price-to-earnings multiple (a common valuation that can tell us how ‘cheap’ or ‘expensive’ stocks are relative to their earnings) for the S&P 500 Index has increased by only one point, from 19x to 20x.

Positioning and asset allocation – we remain overweight risk assets. Since the onset of hostilities with Iran, GDP growth estimates have declined from 2.5% to 2.2% and inflation estimates have increased (Core PCE is now +3.2%, up from +2.4% in January), due to the transmission mechanisms of higher gasoline prices and trade disruption. Despite this, our base case remains an expanding economy, supporting our positioning in risk assets. This includes an overweight to equities (both domestic and international) and an overweight to credit exposure over government exposure within the fixed income asset class.

We expect the US Dollar to continue to weaken. The dollar has continued its multi-year trajectory of weakening as the US debt profile remains high and US alliances – and the dollar demand they have historically generated – have been called into question. These factors are currently offset by interest rate differentials, which support the USD. However, if the futures markets are correct and interest rate differentials increase later this year, the USD would likely continue its multi-year weakening trend. This provides a structural tailwind for international assets, particularly emerging markets.

Fed on hold – for now. At its April meeting, the Fed kept the Federal Funds rate steady at the 3.50%-3.75% range. As he has recently, Stephen Miren dissented from the decision, instead favoring a rate cut. Three other governors also dissented, on the opposite side: they favored removing the easing bias from the language in the statement, although they agreed with the rate decision. Kevin Warsh has been successfully voted out of the Senate Banking Committee, and we expect he will be approved during May. Chair Jerome Powell has said he will stay on until investigations into the Fed are “well and truly over”. His term as a governor runs through January 2028, so he may decide to stay on even as his term as Chair concludes. We believe that given consistently high inflation, the Fed is likely to remain on hold for some time, supporting an underweight to fixed income assets.

A look at prediction markets: Investing? Gambling? Information content?

Beyond analyzing traditional indicators as articulated above, this month we examine how prediction markets work and under what circumstances they can be useful.

Prediction markets, which have grown rapidly over the past few years, are sites where participants buy or sell contracts tied to the outcome of future events. If the event occurs, the participant receives a payout; otherwise, the contract expires worthless. Examples of events commonly bet on are sports scores, election results, and corporate events. Much like financial markets, prediction markets translate the cumulative wisdom of crowds into prices. However, unlike financial markets, prediction markets do not allocate capital; instead, they effectively forecast outcomes. Traditional financial markets also offer ways to forecast outcomes that are not strictly allocating capital; for example, market participants collectively forecast the Federal Funds rate in future months through the futures markets while not allocating capital to the Federal Reserve.

One key difference between prediction markets and investing in a stock or bond is that in aggregate, prediction markets are by definition “zero-sum.” This contrasts with equities or bonds, where the aggregate markets can – and historically have – appreciate over time as equity and fixed income investors earn the returns generated by capitalists and innovation.

Given the zero-sum nature, do prediction markets add value to the economy – or are they economically equivalent to gambling? Although prediction markets do not generate positive financial returns in aggregate, they arguably generate some value by predicting future events with more accuracy than other methods, because they source information from a broad swath of market participants. One could compare them to other predictive processes like polls, expert surveys, or sell-side earnings estimates. Each type of predictive process comes with some built-in weaknesses: polls often have low response rates that must be adjusted for; experts can be overconfident; and sell-side analysts have conflicts of interest that can bias their predictions. Prediction markets likewise have weaknesses: they can be thinly traded, manipulated, or insufficiently broad.

The largest prediction market platforms today are Kalshi (founded in 2018) and Polymarket (founded in 2020), although Robinhood, Interactive Brokers, and other exchanges also offer prediction contracts. Investors are interested: Kalshi recently raised capital at a $22 billion valuation while Polymarket raised capital at a $15 billion valuation. Both companies have signed deals with sports leagues and with news outlets; predictions were displayed on the Golden Globe broadcast.

Prediction markets face some obvious hurdles. Gambling in the US is regulated at the state level, and organizations like casinos and online betting companies have spent a lot of time and money complying with state-level regulations. States, casinos, and Native American tribes have all brought lawsuits against the large prediction market exchanges, claiming they are operating illegally. Like derivatives, prediction markets are regulated by the Commodities and Futures Trading Commission, which under the current administration has taken an intentionally light touch to prediction market regulation. Donald Trump, Jr. serves as advisor to both Kalshi and Polymarket, which may present a conflict of interest.

A few high-profile seemingly well-timed trades have also invited scrutiny: one trader placed highly accurate bets related to Google’s “Year in Search” rankings, and a Kalshi employee who was also working for a prominent YouTuber placed bets on that YouTuber’s behavior. Perhaps best-known is the US Special Forces Army Master Sergeant who placed profitable bets on the timing of the capture of Venezuelan president Nicolas Maduro; he had been directly involved in the mission’s planning.

Analysis by Wolfe Research showed that prediction markets anticipate earnings beats and earnings misses more accurately than the sell-side analyst consensus, reinforcing prediction markets’ claim to harnessing better information than traditional methods.

Who wins and who loses with prediction markets? Since this is a zero-sum game, in aggregate nobody wins financially, although one can argue that more sophisticated traders are likely to make money at the expense of casual traders. Beyond the traders, the platforms win, as they take a fee for each contract bought or sold; this is what supports the high platform valuations. And observers who use contract prices as one piece of a mosaic win, because they assemble a perhaps better picture of the world.

In sum, prediction markets can be useful as one input in an investment process and are an interesting signal in many areas, reminding us that markets can price beliefs as well as cash flows. One should remember, however, that the signal is only as good as the population betting; they can be subject to manipulation; and naïve traders are unlikely to consistently make profitable bets. We view prediction markets not as an investment opportunity but as a probabilistic overlay: useful when viewed with a critical eye, but dangerous if taken at face value.