By Andrew Wetzlel, CFA®, Managing Director of Sustainable Investing

As the Iran conflict grabs attention, with related supply chain dislocations and spiking commodity prices, in the background, the structural growth in demand for power from electrification and AI datacenters continues apace. The conflict is a vivid reminder that the traditional energy system is rooted in instability, volatility, and environmental challenges.

As we’ve written previously, power demand is inflecting higher in the US. While there are a number of demand drivers, AI infrastructure development is front and center. The leading hyperscalers developing AI models and the capacity to deploy this technology understand the challenges this development poses to the power system and the health of our climate. With clearly stated climate goals, these large technology companies have led the investment in and development of clean energy resources. As outlined last July, the US government also continues to support low-to-zero carbon high-capacity power through the OBBBA, including energy storage, nuclear, and geothermal energy. This confluence of factors is driving capital investment and innovation in many areas, with geothermal a growing area of interest.

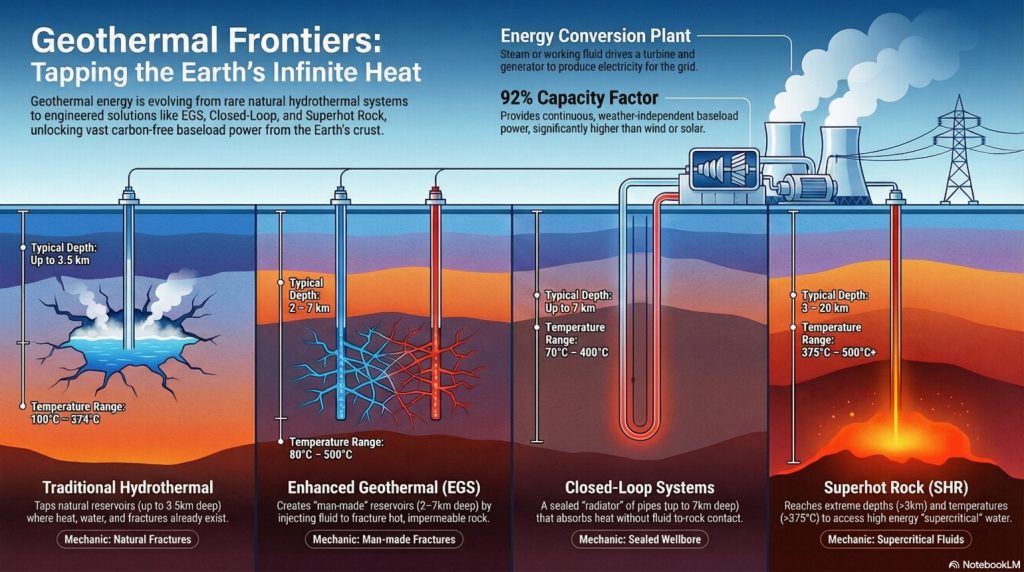

Traditional geothermal, known as hydrothermal power, relies on naturally occurring reservoirs with a specific combination of characteristics: heat, water, and rock permeability. Geothermal systems capture heat from the earth to drive turbines that produce electricity. The specific geologic requirements for conventional geothermal have constrained development historically.

In recent years, a number of start-up companies have developed “next-generation” geothermal (NGG) techniques, that have the potential to significantly expand the reach of geothermal energy. These NGG technologies leverage drilling techniques that create the natural characteristics of hydrothermal projects. NGG has the potential to transform geothermal from a geologically constrained resource to a predictable engineered manufacturing process with vast potential.

There are three NGG techniques in development today:

- Enhanced Geothermal Systems (EGS) is the most advanced of the three. EGS uses horizontal drilling and fracturing to create permeability, though this comes with seismicity-related and water intensity risks.

- Closed-Loop Systems (CLS) use directional drilling and pipes to create a system that virtually eliminates subsurface fluid interaction and seismicity risks, though heat transfer efficiency is lower relative to EGS and costs are higher.

- Superhot Rock Systems (SRS) are earlier stage. SRS has the potential of significantly higher energy density and reduced system footprint, though comes with the technical hurdles of very deep drilling.

There is inherent tension between the development of zero-carbon baseload power at scale and employing drilling techniques developed by the oil and gas industry that present their own environmental risks. Fortunately, drilling- related risks are well understood and the geothermal industry is working to address these in the development phase. A recent paper in Energy 360 Journal outlines risk mitigation measures such as real-time microseismic monitoring, double-walled casing, and 100% reinjections to maintain pressure, among others. Ultimately, the geothermal industry needs to build public trust before scale is possible.

As with all forms of power generation, scale is what matters, and this is achieved through cost reduction. National Renewable Energy Lab (NREL) estimates show that the levelized cost of energy (LCOE) for hydrothermal projects today is about $82 per megawatt-hour (MWh), consistent with Lazard’s LCOE range of $66-$109 MWh. NREL LCOE estimates for EGS currently point to $107 MWh, with drilling costs representing 30-60% of project cost. Private EGS company Fervo has reported a nearly 50% reduction in drilling costs in their Cape Station project, showing that optimizing drilling techniques can significantly improve project economics and timelines. NREL’s more aggressive cost reduction scenario points to EGS LCOE of $45 MWh by 2035. This means that even without subsidies, ESG is likely to be competitive with the lowest cost natural gas combined cycle projects in less than a decade. Add in OBBBA tax credits and geothermal projects could become one of the most cost-competitive forms of new power generation.

While project cost is a critical factor, it’s important to note that geothermal energy plays a different role than other forms of clean energy like solar and energy storage. The large rotating turbines that produce electricity from geothermal heat provide physical inertia that resists sudden changes in frequency and voltage on the grid. This dynamic helps stabilize the grid when there are supply and demand imbalances. Ancillary services like frequency regulation and spinning reserves are increasingly valuable to the grid as intermittent renewable energy is added to the system.

Today there are about 4 gigawatts (GW) of geothermal power capacity in the US. As EGS costs come down rapidly, this zero-carbon dispatchable base-load energy source has significant potential for growth. NREL estimates potential geothermal capacity of 38 GW by 2035, roughly 2% of estimated total US capacity. With a capacity factor over 90%, geothermal could be responsible for over 6% of total electricity generation within ten years.

The largest companies in the Tech sector, the hyperscalers, are actively investing in the commercialization of NGG. Google, in partnership with NV Energy on a Fervo project, is the first Tech firm to receive power from a functioning EGS project for a datacenter. Subsequently, Meta signed a deal with Sage Geosystems for EGS projects in TX, showing that geothermal is breaking away from traditional geologically constrained sites.

Beyond tax incentives, the US government is supporting innovation in EGS through the Wells of Opportunity (WOO) program at the DoE. The WOO program is centered on the evaluation of millions of miles of existing, inactive, or abandoned oil and gas wells across the US for EGS potential. Analyzing for potential ability to retrofit or repurpose for geothermal heat recovery or closed loop systems, the DoE sees potential for 300 GW of EGS by 2050. This would be leveraging historical infrastructure that heavily contributed to climate change to drive the structural architecture of a zero-carbon future. This program could represent the ultimate recycling program for the energy sector.

As we look ahead, geothermal is transitioning from a constrained niche in the power market into a highly scalable manufacturing industry, offering the dispatchability and physical inertia of a natural gas plant with the zero emissions profile of a solar farm. Driven by the deep capital of the tech industry and support from the US government, merging with the hardware innovations of the O&G sector. This is the collision of old school heavy industry and the future data economy playing out in real time.